My last two accounting-focused blog posts centered on related topics. The similar ambition of accountants I’ve observed is a human interest in the good fortunes of others. From there, linking opportunities with resources–“scaling up”–becomes a tangible opportunity for accounting firms via a coupling strategy.

How to Innovate

“So that accounting firms’ clients remain salient, productive, and intelligently profitable,” I wrote in Innovation: Accounting As A Process & Product, “additional professional services to clientele may be…

- “Support beyond bookkeeping, accounting and tax services, and

- “Reconditioning client strategy.”

An article I read in Harvard Business Review takes this idea another step further.

Coupling Strategy

Thales S. Teixeira is the Lumry Family Associate Professor at Harvard Business School. He recently wrote an article entitled “Disruption Starts with Unhappy Customers, Not Technology.” There, he defined what he called a ‘coupling strategy’ as

“…the concept of creating new

products that create

meaningful synergies with

your original product.”

Coupling Strategy

&

Scaling Up

Coupling strategy reflects what I wrote about last time on scaling up.

Teixeira went on to say:

The fastest way to grow is to offer something that your current customers, those most loyal to you, would gladly pay for if you provided it and that, by virtue of them acquiring this new offering, it would make your original product or service even more valuable to them.

A key to understanding the above is calling out what may seem obvious, but could be troublesome. The “meaningful synergies” that “make [bookkeeping, accounting, and tax services] even more valuable…” are from the perspective of the customer, not the accounting firm.

“Meaningful Synergies”

Successful growth is dictated by benefits accrued to the customer, not to the company. After all, it is they who choose whether to adopt or acquire your new products or not.

Thales S. Teixeira, 2019

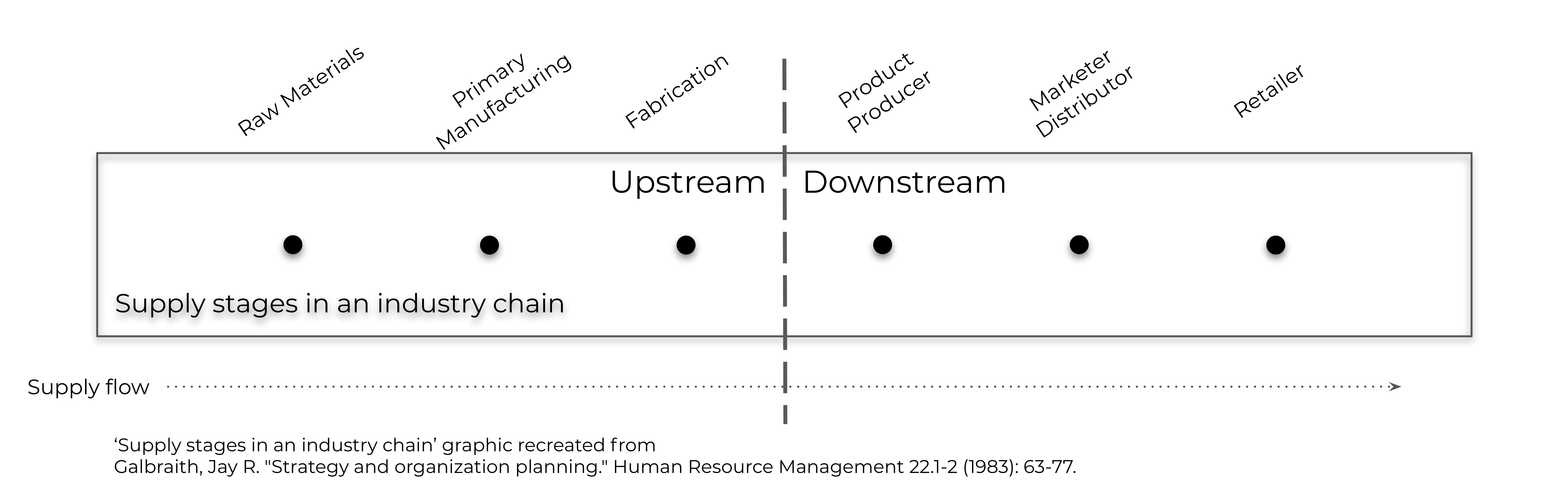

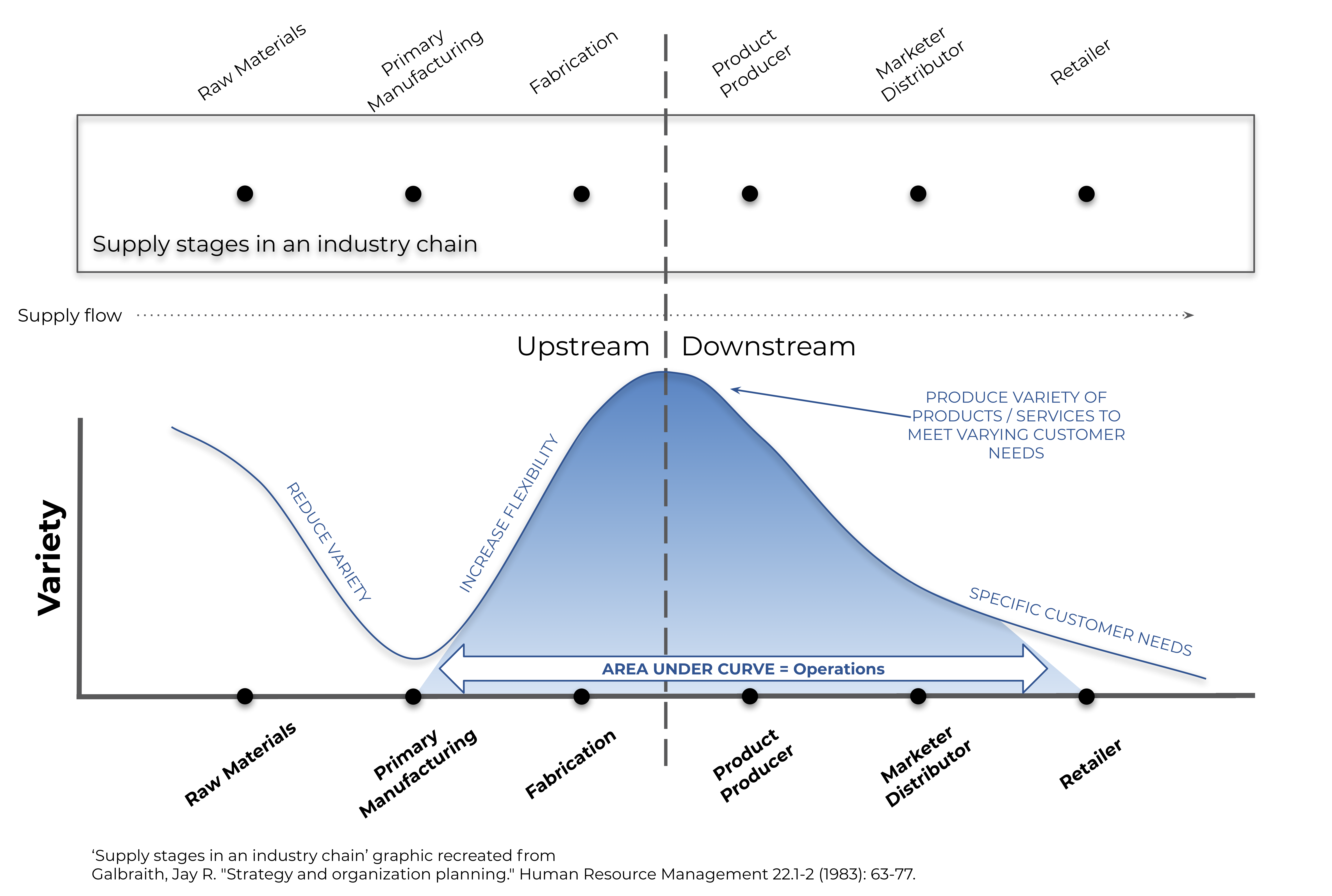

The obvious question is can the accounting firm supply the type of service(s) the customer wants? To figure this out, let’s look at what back in 1983 Jay R. Galbraith called a firm’s “center of gravity.”

The center of gravity of a company depends on where in the industry supply chain the company started.

The mind set of the upstream manager is geared toward standardization and efficiency. They are the producers…In contrast, downstream managers try to customize and tailor output to diverse customer needs.

Jay R. Galbraith, 1983

Accounting for What’s already Happened

With respect to the accounting firm’s client, the accounting firm comes after the supply stages in an industry chain, i.e. off to the right of Retailer. That is, accounting is neither upstream, nor downstream. Those are client operations’ responsibilities. Why? The accounting firm is a data receiver, not a procurer, manufacturer, fabricator, producer, marketer, distributor, or retailer – much less a data generator.

From my Accounting Concerns blog post last week I offered the following remark:

As your tax accountant and/or accounting services provider, I see your financial picture. The numbers generated by your business are “lagging indicators,” or an exhibit of what’s already happened. What if there was a more proactive way to help your business solve problems?

OK, SO WHERE’S THE MEANINGFUL SYNERGY?

Meaningful synergies require an accounting firm to think differently – about itself, its clients, and the delivery of value. What is valuable to the client? Does the accounting firm provide all of that value already? How do we know?

One of the clearest ways to couple is to launch new products or services that are immediately adjacent to (i.e., occur before or after) the activities that consumers already undertake with the business.

Thales S. Teixeira, 2019

There, Teixeira gives us the answer. What happens before the accounting firm gets its data to do its part?

The customer operates.

Then accounting happens.

Is that–the customer operates–too broad of a way to think about what’s adjacent to accounting? The accounting firm’s leadership must ask itself. How much leverage does this firm have over the way the clients’ businesses are run?

If the answer is anything other than None or Extremely Little, then either the firm’s accounting practices are too involved in operations or leadership believes they’re providing more value than is really the case (or the client erroneously believes as much) which comes with ethical concerns.

Frankly, how the clients’ businesses operate is not the accounting firm’s decision. That would be like the accountant telling the restaurant chef what recipes to prepare, or the engineer where a load-bearing wall should be located. Can any accounting firm operate if the client specifies how to run a bank reconciliation? That’s not OK.

Human Interest In the Good Fortunes Of Others

An accounting firm is hired to do accounting. That doesn’t stop the accounting firm’s leadership from caring about their clients. It is, however, possible to serve the needs of the client’s operation, too.

The main hurdle of pursuing the coupling strategy is that this may lead your company into vastly different businesses that require vastly different people, skills, and capabilities than the ones your company possesses.

Thales S. Teixeira, 2019

Rehr Consulting

In a 30-minute to 1-hour informational interview (in person, telephone call, Skype, etc.) I would get the answers to 3 basic questions:

- Why did you get in business in the first place?

- What are your Top 3 goals, and Top 3 risks?

- Is your business operating in alignment with your personal ambition?

From there, I would work with that client to figure goals, devise ways to achieve the desired business performance (strategy), and strengthen resilience.

Teixeira, T. (2019). Disruption Starts with Unhappy Customers, Not Technology. [online] Harvard Business Review. Available at: https://hbr.org/2019/06/disruption-starts-with-unhappy-customers-not-technology [Accessed 11 Jun. 2019].

Galbraith, Jay R. “Strategy and organization planning.” Human Resource Management 22.1‐2 (1983): 63-77.

Leave a comment